by bexadmin | Apr 17, 2026 | Recent Events

By Roland Murphy for AZBEX – BEXclusive The Public Works event in the BEX Leading Market Series is consistently one of the best attended every year, and 2026 proved to be no exception. Nearly 150 people signed up to come to SkySong on April 14 and hear the...

by bexadmin | Mar 6, 2026 | Recent Events

By Roland Murphy for AZBEX – BEXclusive Anyone who has ever stepped into a new role knows the challenges, thrill and trepidation that come with taking the reins and making that slot your own. Whether the role is newly created, meaning your actions will influence the...

by bexadmin | Feb 6, 2026 | Recent Events

By Roland Murphy for AZBEX The dominant theme and mood for the Arizona construction market heading into 2025 was uncertainty. Major changes in federal policies, expected shifts in population growth, nearly every economic indicator up in the air, increases in organized...

by bexadmin | Dec 19, 2025 | Recent Events

By Roland Murphy for AZBEX – BEXclusive The Higher Education session of the BEX Leading Market Series is always one of the year’s best attended, and 2025 proved no exception. The audience for the Dec. 16 event was treated to a panel moderated by Cassie Saba, Arizona...

by bexadmin | Nov 14, 2025 | Recent Events

The BEX Healthcare Leading Market Series event is almost always the best attended of the year, and the capacity crowd this week at SkySong showed that trend is continuing. Sponsored by Kitchell Corporation, this year’s panel focused on the changes in development and...

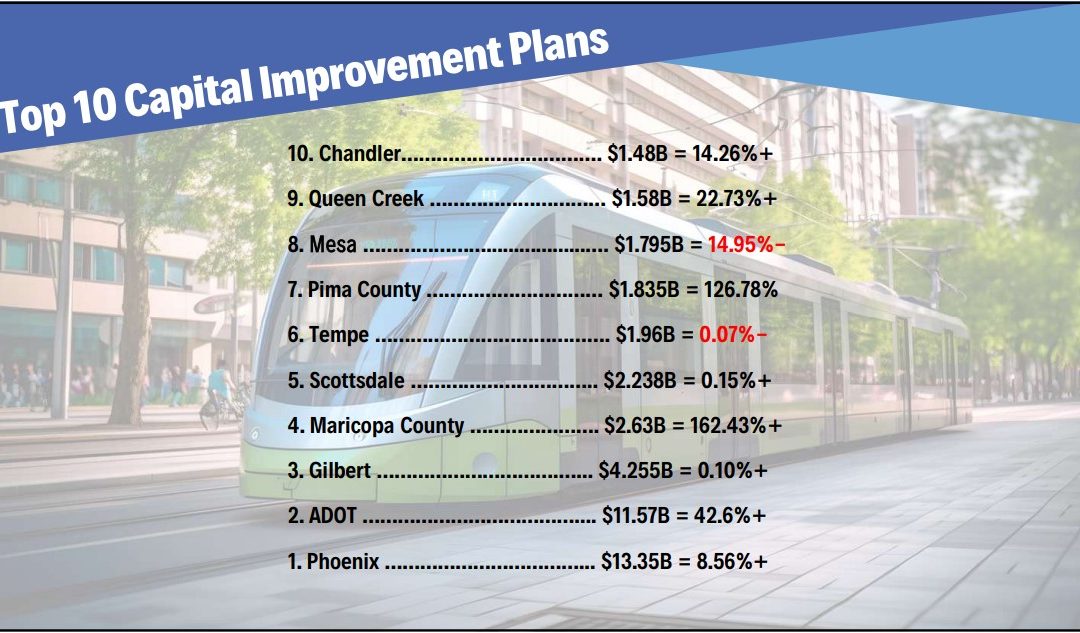

by bexadmin | Oct 31, 2025 | Recent Events

More than 200 attendees packed the Desert Willow Conference Center in Phoenix this week for the BEX 2025 Public Works Conference—the year’s most comprehensive discussion on public construction and development projects in Arizona. Master of ceremonies Jamie...

STEVE BOSCHEN

STEVE BOSCHEN WENDY COHEN

WENDY COHEN ERIC FROBERG

ERIC FROBERG

REBEKAH MORRIS

REBEKAH MORRIS